How can insurers use insurtech opportunities?

How can insurers use insurtech opportunities?

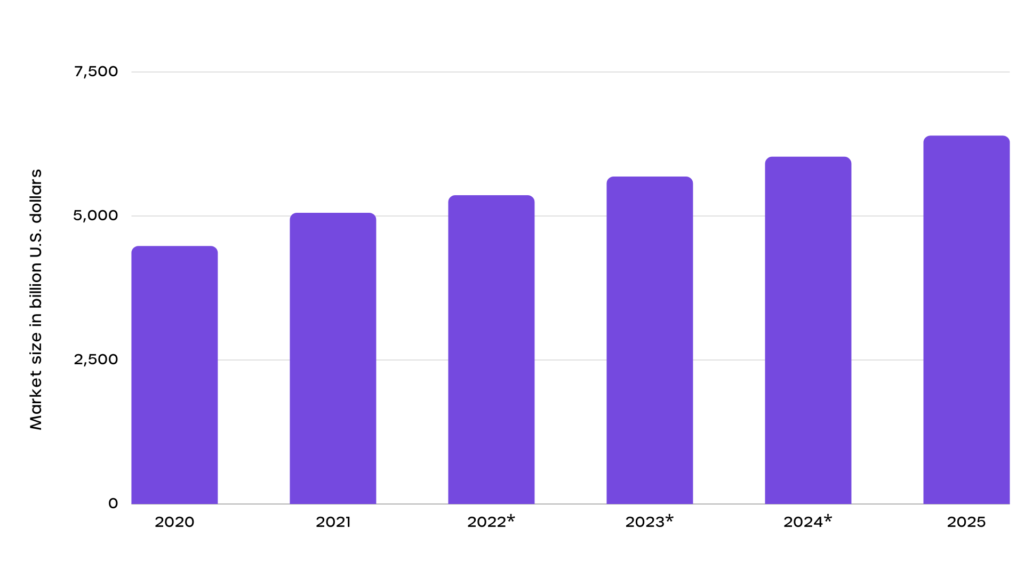

Cyvatar | 03/24/2022The insurance industry has shown tremendous growth in the last few years (expected to reach $6.4 trillion in 2025)

Every time there is a new technology trending, the insurance industry has embraced it and evolved.

They have managed to respond with new products, new distribution channels, and smarter ways to evaluate risks.

The latest technology entrants have upended assumptions about how the insurance industry functions: operating models, structures, market strategies, and the whole business itself.

This is where insurtech becomes one of the biggest game-changers for the insurance industry.

What is Insurtech?

Insurtech refers to everything which connects technological and digital innovation within the insurance sector.

With insurtech, getting insurance quotes could be achieved with a single click, claims will be processed in minutes, customers can get highly personalized insurance products, and so on.

Thanks to its agile structure, insurtechs are proving themselves to be excellent at meeting customer demands.

How is Insurtech different from legacy IT systems?

Insurtech doesn’t require legacy IT systems and processes. It uses the latest suite of technologies to design digital processes, systems, products, and services, from scratch.

Insurtech leverages digital tools to provide value. Let us look at how insurtech is different from the traditional technology for the insurance industry.

1. Provides full automation

Thanks to an automation-only approach, insurtech accelerates processes and cuts costs significantly to meet customer expectations.

McKinsey claims that 50 to 60 percent of back-office operations can be automated.

2. Data-driven decision making

Since the IT systems have access to varied sources of data, insurtech applies machine-learning techniques to offer personalized products and services.

3. Targeted products

Based on the usage or as value-added services, insurtech offers personalized small-ticket products. For example, a customer who is renting a car can purchase insurance only for the hours that they use the car.

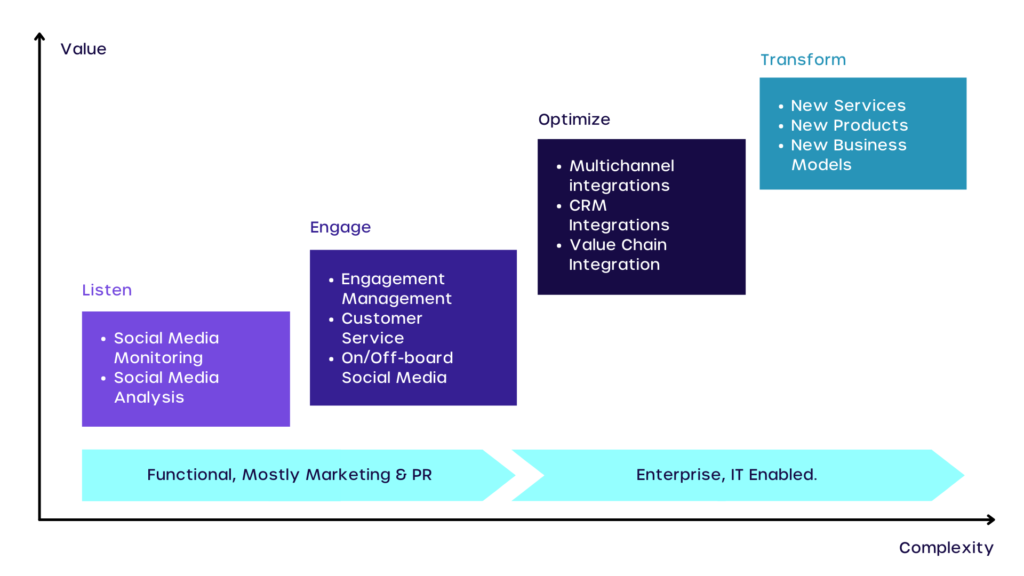

4. Better social engagement

Insurance companies have started to use social media as a disruptive advantage and leverage on the social media maturity curve.

Insurers can connect different social channels to their CRMs to listen to their customers and hence, better serve them. This could help them segment their audience and provide customized insurance solutions.

Insurers can leverage social media maturity to transform the way they interact with their audience.

With the help of insurtech, insurance organizations can now use complex AI and IT-enabled social media tools to better position themselves and stay competitive.

5. More customer interactions

Some insurance companies offer a new-age suite of technologies that lets consumers connect with them.

For example, AI-powered chatbots provide a 24/7 service, and they are also able to answer complex queries.

6. Digitized ‘moments of truth’

If insurance companies don’t handle customers’ pain points, it can severely dent their trust in the former. There are insurance products whose specific solution is to solve the issues of the customers.

For insurance companies that are only using legacy IT systems and infrastructure, you don’t have to worry.

Insurtechs are not looking to replace traditional insurers. They are focusing on digitizing parts of the insurance value chain.

Traditional insurers have to assess their business pain points to understand which area of their value chain can be enhanced with the help of insurtech.

Benefits of Insurtech

Let us look at some of the benefits of insurtech for both consumers and insurance companies:

1. Insurtech for the Consumer

Insurtech allows the inclusion of family and friends (called friend assurance) to get comprehensive coverage.

In the insurtech landscape, consumers are part of every process, starting from registration to claims, and this enhances their engagement.

Since most people always have a mobile phone handy, it becomes easy for them to conduct transactions as insurtech is mobile-friendly.

Insurtech companies have strict security policies, follow a set of regulatory compliances, and have protocols that ensure the safety of customers’ data. Since they also collect data from customers, they suggest data-driven products and solutions.

2. Insurtech for Insurance companies

Keeping fraudulent claims at bay saves time and money for itself. The Know Your Customer (KYC) process is seamless in insurtech for insurers.

Since it automates information collection, it simplifies the process of underwriting. It is estimated that by 2030, underwriting will cease to exist.

Insurance companies can introduce newer models of insurance distribution such as peer-to-peer insurance, thanks to the advanced technologies that they use

Owing to such benefits, traditional insurers have started to adopt insurtech.

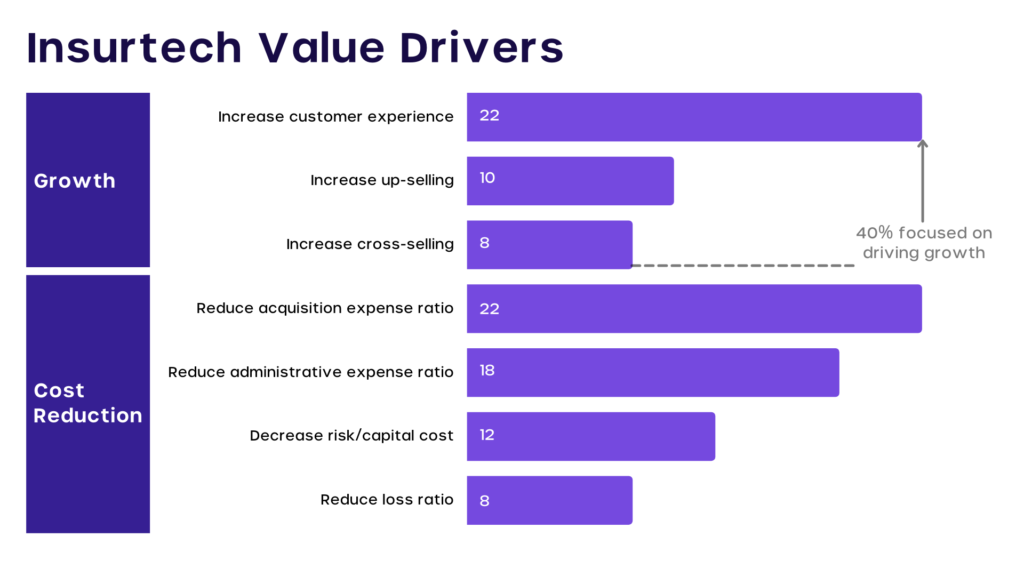

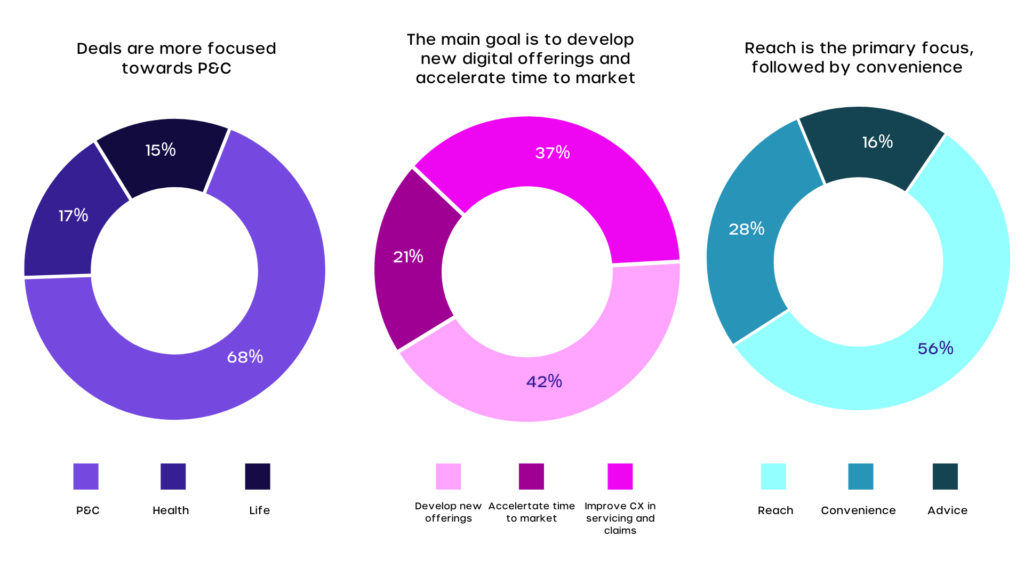

Per the recent 2021 Capgemini analysis, more than half of the incumbents sought insurtech partnerships to expand reach.

This analysis was made looking at the partnerships and acquisitions of the 15 largest insurers globally- 44 deals in 2020 and the observations were made of 3 categories:

1. Business Lines

Property and casual insurers still account for the lion’s share of the capability enhancing deals (68%), followed by health insurers (17%) and life insurers (15%).

2. Deal Goals

Developing new digital offerings such as on-demand or pay-per-use insurance was the most common objective of these deals (42%), followed by accelerating time to market (37%). Interestingly, only 21% of partnerships/acquisitions focused on improving service or customer experience for claims.

3. CARE Impact

Improving Reach was the primary goal of 56% of these deals, followed by Convenience (28%) and Advice (16%).

How can Insurers use Insurtech opportunities?

Insurers spent around $225 billion on IT, in 2019. The pandemic did slow down investments, however, the trends are indicating that insurers will start spending more to rejig their IT infrastructure.

McKinsey says that 9 out of 10 insurance companies identified that their legacy systems and infrastructure are barriers to digitalization.

It is clear that there is an urgent need for insurance companies to adopt the latest technologies on a war footing.

Let us look at what the insurance companies stand to gain if they adopt insurtech:

1. Managing Claims

Insurance companies can leverage blockchain technology to create a standard claims document evaluated by underwriters in real-time.

It can also automate smart contract elements, thereby ensuring that its execution is transparent, thanks to blockchain’s ledger-based technology.

It forges the relationship between insurers and consumers. McKinsey estimates that by 2030, more than half of the claim activities will be replaced by automation.

2. Know-Your-Customer (KYC) Verification

One of the most important aspects of the customer verification process that insurers should compulsorily complete is the KYC process.

Insurers will have to collect all information to verify the identity of the applicants- and it will amount to huge volumes of data. Insurtech acts as the savior here.

Some insurtech companies have used Blockchain to develop software that stores customer identification details. Banks can save at least $12 million every year by improving their KYC systems.

The savings would come through fine avoidance, customer retention, and reputation management.

3. Smart Contract Formulation

Smart contracts are a Blockchain-powered technology that verifies and executes the transactions between parties.

It helps both the insurers and customers to manage claims transparently. It eliminates the need for a claims assessor since the claims are automatically enforced by computer protocols.

Since contracts and claims are recorded in the blockchain and ratified by the network, it ensures that only valid claims are paid.

With better claims handling, customer experience also improves by a huge margin.

It eliminates processes such as document submission and third-party verification. It also speeds up the underwriting process and reduces the costs involved.

4. Tokenized Insurance

It represents the ownership of a policy by using digital tokens. These tokens can be used to make payments on a policy, redeem them for future payments, or to receive dividends.

5. Fraud Detection and Risk Prevention

The FBI estimates that the total cost of insurance fraud is around $40 billion every year, and it costs the average American family between $400 and $700 per year.

Fraud is a big problem since high-value assets can be claimed as stolen. By providing a centralized digital repository, blockchain increases the chances of detecting fraud.

It can independently verify the claims of the customers and provide the entire transaction history.

Therefore, it becomes easy to prevent transaction duplication and provide a verifiable record of all the transactions.

Many insurance companies are already using blockchain for reducing fraud and the liability that is associated with payments.

Since there is an independent record of all transactions, it has the potential to stop many fraudulent activities.

In 2020 alone, financial institutions incurred a fine of over $10.4 billion for data privacy, anti-money laundering, and data privacy.

6. Personalized Insurance Pricing

The traditional method of risk assessment was based on datasets that were not personal to the consumer.

Thankfully, large amounts of data are sourced by insurers to get better risk assessment, happy clients, and stable margins.

A study by Accenture says that three-quarters of consumers are ready to share their personal data if they can get cheaper risk coverage.

Underwriters can leverage a variety of highly personalized records. The advent of connected devices has enabled deeper insights into the physical condition of the customer.

Insurers can even monitor customers’ lifestyle patterns based on the number of steps they take every day and the number of hours they get to sleep, through data collected from the fitness tracker.

7. Telematics Insurance

It is a form of auto insurance policy that uses in-car tracking devices to track the vehicle’s mileage, speed, driving time, breaks, and other factors, to calculate the policyholders’ insurance premiums.

The device includes motion sensors, SIM cards, and analytics software.

The system processes the information and shares it with the insurtech insurance company for analysis. Driver behavior analysis is used to create personalized insurance plans and to improve risk management.

In the event of a car accident, insurance companies can increase charges for erratic driving.

The telematics market size is expected to reach $13.78 billion, by 2030. Only 6% of Americans are enrolled in an insurance telematics program, however, the number will only keep increasing.

Telematics will be a huge enabler for disruptive business models such as pay-how-you-drive (PHYD), pay-as-you-drive (PAYD), and usage-based insurance (USBI).

8. Peer-to-peer (P2P) Insurance

In this model, a network of people agrees to have cover for the same risks by creating a unified finance pool consisting of premium shares.

The P2P model doesn’t require the presence of insurance companies at all. Yulife, Pineapple, Nexus Mutual, and Friendsurance are some of the popular startups in the P2P insurance space.

Considered one of the most disruptive models, P2P insurance reduces costs and mitigates claim conflicts.

After the coverage period ends, the available money is refunded. Even though this model has a few drawbacks, there are a number of startups that are already focusing on this.

9. Cyber Liability

It focuses on the integrity of the digital assets that belong to a particular network. It includes switches, routers, data point configurations, etc, for real-time verification of the state of the network.

Let’s take a look at a case study of how a multinational insurer reduced the risk assessment process time from days/weeks to a couple of minutes.

CASE STUDY

| Productivity-enhancing digital solution sparks new relationship model for insurer and hospitality clients Madrid-based MAPFRE is a multinational insurer with 23 million clients worldwide. It is Spain’s leading insurer and the largest non-life insurance company in Latin America. Hospitality coverage, one of MAPFRE’s highest-volume business lines, has become increasingly relevant. BUSINESS OBJECTIVES AND CHALLENGES: The hospitality sector was hit hard by lockdown and mobility restrictions over the last year. Through a field study of hospitality-business policyholders, MAPFRE learned that risk identification and assessment processes were friction-inducing. Business owners/executives perceived their first contact with the insurer to be slow and frustrating. Typically, issuance for a hospitality business was manual, tedious, and complicated, which caused long response times. Moreover, each business is unique with distinct needs. The challenge was to develop an agile, cross-sector solution that made insurance more friendly, adapting the processes to the new reality, digitizing the underwriting and verification processes, empowering agents and clients by replacing management complexity with a digital approach, offering clients greater transparency to the insurer’s decision making, and offering a better user experience. SOLUTION: MAPFRE leveraged customer-centric methodologies, incorporating client perspectives to validate the field study insights. The result was a Digital Assessment solution that enables rigorous and agile data collection to verify risks. The solution includes image recognition modules with geolocation technology and predictive modeling for a differentiated customer experience. After receiving a web link, policyholders access the application, and a virtual assistant welcomes and guides them through the process. Integrated geolocation and zoning data enable quick identification of affected premises. Then, the hospitality business owner shares photos and business details. The Digital Assessment solution automatically reviews several risk elements, analyzes images, messages the client and insurance agent to confirm verification, and allows issuance to proceed. BENEFITS/RESULTS: MAPFRE reduced risk assessment process time from days/weeks to only eight minutes. Also, with rich information from the images and other data sources for underwriting, MAPFRE now gains intelligence and criteria to best suit each client’s needs. |

Barriers for Insurtech

One of the biggest barriers for insurtech is the privacy factor. Blockchain’s distributed ledger technology is publicly available and is shared across multiple financial institutions to keep track of credit scores and transactions.

Given the decentralized nature of blockchain technology, no organization will be held liable if there are any disputes.

Since it constantly keeps changing, it poses an issue for data protection laws. There are jurisdiction concerns as well when it comes to privacy.

Regulators across the world are also taking different approaches when it comes to regulating blockchain, therefore, it becomes difficult to gauge how the system will be supervised.

With more and more data flow, the systems could be overloaded, causing quality and privacy issues. It could also pave the way for cyberattacks.

There are worries that insurtech can cause inequality. How?

There will be some parts of the world that will be in an advantageous position to get reduced insurance services compared to others- it can deepen the inequality.

Some of the above reasons might act as a barrier for us to see greater innovation in insurance products.

How Startups Can Use the Cyvatar + Cysurance Solution

There are always some risks involved with individuals or organizations in anything they do; be it online or offline.

Cybersecurity services are no exception. We know the risk and hence, we have best-in-the-class cybersecurity security.

That said, we proudly provide insurance with our managed security services. We partner with Cysurance to build enhanced cyber assurance and ransomware prevention into our subscription packages. This covers losses up to $100,000 for our Cybersecurity Foundations and Cybersecurity Prevention members.

| Learn more about ransomware prevention and Cyvatar’s effortless cybersecurity: CSaaS pricing |